5 Levels of Savings

- Vincent Chua

- Jan 6, 2020

- 6 min read

If one of your new year's resolutions is to have more money, then this post may be especially useful for you.

Below is how I view the different aspects of savings.

Saving money is one of our core values for most Asians,

Probably because our ancestors had a very difficult time; hence, most of them are very good savers. And thankfully, they continue to pass on this good tradition of savings to the following generations.

As our society and financial earning capacity improve, we start to get more comfortable. Many of us have numerous buying choices now, which leads me to my first point...

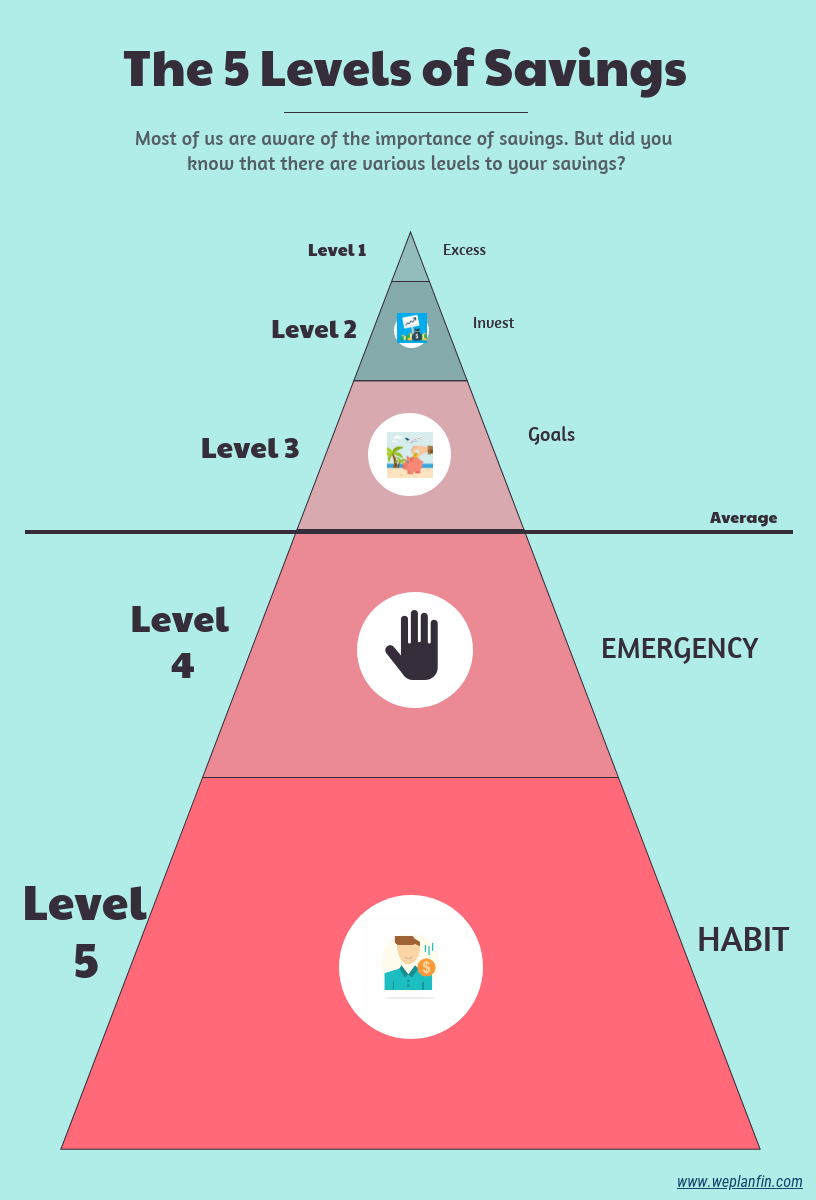

Level 5: Habit

Or more accurately, spending or saving habits.

I won't be telling you what you should spend or save on. I believe most of us can differentiate between what we need and what we want.

(If you can't distinguish the difference, then I strongly suggest you find yourself a personal finance coach to help you with this.)

One quick tip is to save before you spend. And not spend and save what's left. Chances are, there wouldn't be much left at the end of the month.

And we can only move up the economic ladder when we save a portion of what we earn. Otherwise, you will find yourself in a rut very soon.

Couldn't have put it better than the famous actor for the inspiring movie, "Pursuit for Happyness"

Too many people spend money they haven't earned, to buy things they don't want, to impress people they don't like. --- Will Smith

If you belong to this category, don't worry. At least now you know your problem. Awareness is the first step.

Once you have the awareness, you can take steps to stop the problem.

Again, if you don't know where to start, you can look for a personal finance coach to help you.

On the other hand, if you are only spending on daily necessities but still find it hard to save money, then your problem isn't about saving.

It's about your income. So look towards learning or improving your skill, getting a new job that pays better, partaking in some gigs on the sideline or marrying a rich spouse (if that is still applicable to you).

1. Higher income, same spending = savings

2. Higher income, higher spending = no savings (not good)

If you had higher spending due to a sudden change in circumstances, then you should read the next point.

Level 4: Emergency

The emergency mainly comes in two main forms:

unforeseen circumstances (like the death of the sole breadwinner, disability or illness)

retrenchment

(I wanted to add a third category called unexpected baby, then again, the process of making it is already in the known, so...I think you get my point.)

As such, it is important we start planning to the best of our abilities for these emergencies.

We have tools like insurance to protect against the first scenario.

And we commonly hear people say we need to have 3 to 6 months' worth of expenses in the bank. The reason for that 3 to 6 months of expenses is because that is usually the amount of time needed to get the next job.

Please note that getting the next job doesn't necessarily mean you will get back to the same job at the same pay. More often than not, when a retrenchment hits, either the market isn't doing well, so most people are laid off, OR your pay is too high for your company to afford you doing that work which can be done at a cheaper price.

As such, we need 3 to 6 months to get another job, which may or may not be a pay cut. It is HIGHLY dependent on your skillsets, mindset and the market at that juncture.

If you don't have the necessary buffer to tide you through this transition, you may be inclined to settle for the first offer that comes your way, which may not be the ideal one you are looking for.

Level 3: Goals

You may have noticed that I had added an extra line of average. I put that in because I find that people are saving for their goals, are in a very fortunate situation.

I stay in one of the mature estates where I know of senior citizens who are destitute. As such, always appreciate and be grateful that you are in this category.

Coming back, goals can be broken down to

short term (a year or less)

mid-term (3 to 5 years)

long term (5 or longer)

It sounds stupid, but it's true. Say you are saving for the year-end trip to Europe, then that belongs to the short term goal.

Mid-term goals are likely property initial deposits, renovations or marriage etc.

Long term goals are likely children's education, retirement or business seed funding.

Therefore, it is very crucial you identify your goals before you choose your vehicle. It is foolish to be choosing a risky high return vehicle if your goals are short term. You are asking for trouble.

Case in point, back in 2007, I had a goal of going to Omaha to attend Berkshire Hathway Annual General Meeting in the following year. I was still studying then and no one was sponsoring me.

What I did was exceptionally ludicrous. I poured all my savings into the stock market and collected a lot of penny stocks.

When the Global Financial Crisis hit in 2008/ 2009, I got washed out and suffered heavy losses. I felt like I was caught pants down.

As a result, I was much further from my goal than before I had invested. I learned an important lesson that year.

To make lots of money in a short period of time, you either have a very huge capital or you choose a higher return vehicle. However, in my situation, the latter wasn't true.

This is because of the saying "high risk, high..."

The only exception to this rule is time. As aptly put by Ann Wilson,

It is not about timing the market, but time in the market.

Hence, choose your vehicles based on your goals and timeframe. Not the other way round.

Level 2: Invest

The first thing that comes to mind is likely investing in the bonds, stocks or properties.

I agree those are very good assets to invest in.

I do want to point out a common blindspot. It's called investing in yourself.

The best gift you can give your future self is not more money. Rather, it's knowledge and wisdom in my opinion.

People can take away your money but they can't take away the intangibles.

Too much money can also be a problem. Much like Warren Buffet. He had so much cash on hand that he has difficulty finding good companies to invest in.

The best investment is investing in yourself so you can have more knowledge and wisdom to decipher the best vehicle for your goals.

Level 1: Excess

If you are in this category now, I would like to congratulate you.

That is where you are at the pinnacle of the financial game. As Robert Kiyosaki, the famous author of rich dad poignantly puts

Financial freedom is the freedom from fear.

This is because you have put aside enough for an emergency, you had achieved some of your goals, your money is working for you and yet, you still have more than what you need.

As such, to me, it's not about how many zeros there are in the bank account. It is about you are no longer worry about money in any circumstances, good or bad.

TL;DR

If you had been scrolling through quickly, here's the wrap-up.

Level 5: Create a savings habit (if you haven't already done so)

Level 4: Have an emergency fund (3 - 6 months of expenses)

Level 3: Set goals. Life is too short to always be saving and not enjoying.

Level 2: Remember to invest in yourself.

Level 1: Having more than what you need or want, resulting in excess (the pinnacle of the financial game)

And if you need any help at Level 3 and/or Level 4, there is an investment talk I have on 31 Jan. I'm not the speaker but I believe you can benefit much from this event.

Whatsapp me (by hitting the bottom right button) or use the chatbot (if you're using a desktop or laptop, also on the bottom right) for more details.

Wishing you an awesome 2020!

Comments